The Rules of Advertising Have Changed: Key Takeaways from the eMarketer Ad Buyer Strategies Summit

Last week's eMarketer Ad Buyer Strategies Summit in New York City brought together a room full of brand leaders, agency executives, and media buyers navigating what comes next in advertising.

As digital ad spend continues to grow, 2026 marks a major inflection point as alternative platforms are set to exceed $100 billion for the first time. Platform giants maintain a strong grip, but the growth of competitive forces signals a fundamental change in how marketers need to think and operate.

AI Has Collapsed the Purchase Funnel and Most Brands Are Still Catching Up

AI was a core theme that cut across nearly every session, because it has compressed the consumer journey from discovery to purchase in ways that most organizations haven't fully absorbed yet.

Tools like ChatGPT are now influencing product decisions before a brand ever gets the chance to serve an ad to the customer. By next year, the average adult is expected to spend 23 minutes per day with AI, and by 2029, it’s expected that $26 billion in commerce searched will be AI-influenced. Ultimately, these shifts in behavior are elevating AI as a primary advertising channel.

But there's a larger issue at play when it comes to attribution. Consumers are reading AI overviews, immediately knowing what they want, opening a new tab, and going straight to a brand's website — cutting publishers out of the opportunity to get compensated and leaving brands unsure where their traffic is actually coming from. Liane Nadeau, Chief Investment Officer at Digitas, put it simply: brands not present in LLMs lose the connection at the moment it matters most. That means thinking about paid, owned, and earned holistically to ensure you show up in AI-cited content — otherwise, you risk being cut out of the discoverability phase entirely.

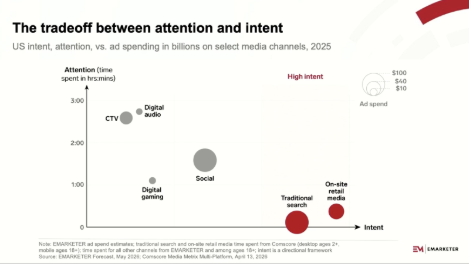

Attention Doesn’t Equate to Intent, Especially in a World of Platform Coexistence

At the core of digital advertising is a strategic balance between attention and intent. Sarah Marzano, Vice President and Principal Analyst at eMarketer, mapped out where different channels fall across that spectrum.

Look at digital audio and CTV for example, which command massive consumer attention and high reach, but users are passive, showing up for content and entertainment rather than to make a purchase. On the other hand, traditional search and retail media work opposite — users don’t spend much time there, but when they do, they arrive with high-intent. This is critical to understand because attention and intent cannot be used interchangeably, especially with the rise of new platforms like AI chatbots.

What makes this harder is that the rise of new platforms isn’t replacing old ones, so advertisers need to have a plan for coexistence. The data keeps reinforcing this: AI isn’t killing search (in fact, time spent on Google has increased in recent years as AI usage grows), CTV is building alongside linear rather than dismantling it, and ChatGPT won't replace retail media.

Advertisers need a plan for coexistence, not just adoption.

That means media buyers need to ask where each channel sits on the attention-to-intent spectrum, and whether consumer behavior in that environment actually matches what a campaign is trying to accomplish. Technical capability does not dictate consumer behavior — and brands that conflate the two will keep misallocating budget. Instead, they must focus on creating habitual destinations for audiences as an anchor in the increasingly fragmented landscape.

Where Measurement Breaks Down

Across sessions, measurement emerged as a persistent frustration with marketers under pressure to prove return on investment to CFOs. One of the most prominent examples is incremental ROAS. Brands have transitioned to focus on incrementality to prove causality, but research from Albertsons Media Collective uncovered that iROAS can swing results by as much as six times depending on the methodology used to calculate it. For advertisers working across ten or more retail media networks, the iROAS metric can’t be compared across retail media networks because the data is incompatible.

The same problem applies to measuring AEO and GEO, compounded by zero-click discovery, bias in LLMs, and brands' inability to control the lag between when training models launch and when AI results reflect their efforts. As Jennifer Mennes, Vice President, Global Head of Digital Marketing & Strategy at Mondelez International said, “This is a boardroom conversation with what I’d say is a very entry-level understanding of the complexity that these spaces need to be invested in.”

The summit's consensus was pragmatic that ad leaders cannot wait for a silver bullet metric. Triangulate across multiple data points, hold partners accountable for explaining their methodology rather than just their numbers, and focus energy on producing quality content that influences LLMs rather than chasing ROI from metrics that don't yet exist. While efficiency tells you what happened, measurement tells you why — but focusing on overall brand health as measurement is being determined is a critical step.

The Next Era of Media Buying Is Cross-Channel and Fluid

The brands and agencies showing up most effectively right now have stopped organizing their media investments by channel and started organizing them around the consumer.

Think about YouTube. It’s the number one place people consume video, but it lives in a social budget. Pinterest is still categorized as social, despite the fact that most users no longer interact with others on the platform. The behavioral reality of how consumers move across platforms has outpaced the way agencies and clients are structured to buy against it, creating an inefficiency gap between how consumers behave and how budgets are allocated.

With the rise of AI, the path to purchase is increasingly fluid, yet most brands and agencies aren't at the point where spend moves fluidly between channels to match. The ones that win will be the ones that think about advertising holistically across the entire ecosystem — paid, earned, and owned — rather than optimizing each channel in isolation.

The Real Competitive Advantage Hasn't Changed

All these forces at play are ultimately changing the value agencies bring today. But at the root of it all remains building experiences that earn their way into consumers' lives. The marketers best positioned to navigate this moment aren't the ones chasing every new platform or waiting for a perfect measurement framework to emerge.

Even amid all the disruption, the fundamentals haven't changed as much as the headlines suggest. The differentiation comes from human-led strategy — the creative thinking, brand judgment, and consumer understanding that gives tools something worth deploying. Roles will continue to be reshaped, and the agencies and brands that recognize that distinction will be better equipped to lead through what comes next in advertising.

What our clients say

Ameresco

Leila Dillon, SVP, Corporate Marketing and Communications

It's clear that the Greenough Communications team has a deep understanding of the clean tech and climate transition spaces. Within the first month of working together, they were able to land interviews with The Washington Post, The New York Times and Canary Media, just to name a few! Since working together, we've seen our media coverage and quality increase significantly across the board. We value Greenough's partnership are looking forward to our continued work together.

Boston Micro Fabrication

Laura Galloway, Marketing Director

As a small marketing team, having an agency partner that feels like a true extension of my team is invaluable. The Greenough Communications team is professional, responsive and has taken the time to understand our business, putting our brand in front of the customers who matter for our growth. I’ve been very happy with our first year of partnership and look forward to future success.

Acrolinx

Mariana Just, Vice President, Marketing

We started working with Greenough Communications over a year ago, and it's been a fantastic journey. They really understand who we are at Acrolinx and what we want to say. Their ability to amplify our message in a crowded AI space has been impressive, delivering solid media results in the outlets that matter, securing the AI Breakthrough Award, and boosting our executive team's social media presence. As we continue our partnership, we're excited about expanding our reach and market presence, building upon our refreshed positioning and messaging with Greenough's expertise guiding us every step of the way.

IQE

Steven Curwood, Director of Corporate Marketing

At IQE, one of our goals is to demystify the vital role compound semiconductors play in the industry and the future of innovation. As we aim to broaden our brand's reach in the U.S. market, finding an agency that understands our technology and the intricacies of our work is crucial. Greenough Communications stood out as that agency from the start. In the short time we've worked together, they've already validated our choice with opportunities in key media, including CNBC, NPR, and the U.S. trade media that will move the needle for our brand and message. There's much ahead for us, and we're excited to have the Greenough team by our side.

Arbella Insurance

John Donohue, CEO

Our Greenough team has excelled in learning our business and our challenges and has been extremely effective in developing and executing a PR strategy that helps drive our success.

Wolters Kluwer Health

André Rebelo, Global Marketing Communications & Public Relations

Our Greenough team has been a strategic asset in sustaining targeted growth in our PR and external communications. The team really operates like an extension of our internal team, aligned and effective. They've deftly balanced the needs of multiple sub-groups' objectives and needs, getting great results in the publications our customers read.

GlobalFoundries

Laurie Kelly, Chief Communications Officer

Greenough Communications has been more than just a PR agency for us at GlobalFoundries; they've been true partners. From navigating our IPO to driving impactful education campaigns like the one leading up to the passage of the CHIPS Act, they've been instrumental in showing the world our leadership role in this new technology era. Their knack for building connections with the industry and our team, including our executives, has been impressive. Every year, we throw new challenges their way, and they keep delivering. As we move ahead together, we're excited to keep pushing the boundaries, sharpening our brand narrative, and taking our brand awareness to the next level.

Integrated Marketing

Content Development

Public Relations

Brand Strategy

Integrated Marketing

Content Development

Public Relations

Brand Strategy

Public Relations

Brand Strategy

Integrated Marketing

Content Development

Public Relations

Brand Strategy

Integrated Marketing

Content Development

Let's start a project together.